UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐

Check the appropriate box:

|

☐ |

|

Preliminary Proxy Statement |

|

|

|

|

|

☐ |

|

Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

|

|

|

|

|

☐ |

|

Definitive Proxy Statement |

|

|

|

|

|

☒ |

|

Definitive Additional Materials |

|

|

|

|

|

☐ |

|

Soliciting Material under 14a-12 |

![]()

CLS HOLDINGS USA, INC.

(Name of Registrant as Specified in its Charter)

(Name of Persons(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

|

|

|

|||

|

☒ |

|

No fee required. |

||

|

|

|

|||

|

☐ |

|

Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

||

|

|

|

|

||

|

|

|

1. |

|

Title of each class of securities to which transaction applies:

|

|

|

|

2. |

|

Aggregate number of securities to which transaction applies:

|

|

|

|

3. |

|

Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined):

|

|

|

|

4. |

|

Proposed maximum aggregate value of transaction:

|

|

|

|

5. |

|

Total fee paid:

|

|

|

|

|||

|

☐ |

|

Fee paid previously with preliminary materials. |

||

|

|

|

|||

|

☐ |

|

Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a) (2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

||

|

|

|

|

||

|

|

|

1. |

|

Amount Previously Paid:

|

|

|

|

2. |

|

Form, Schedule or Registration Statement No.:

|

|

|

|

3. |

|

Filing Party:

|

|

|

|

4. |

|

Date Filed:

|

IMPORTANT REMINDER TO VOTE YOUR PROXY

May 13, 2019

Dear Stockholder:

As of the date of this letter our records indicate your vote has not yet been received for the Special Meeting of Stockholders of CLS Holdings USA, Inc., which is scheduled on June 4, 2019 at 1:00 p.m., Eastern Time. Please take a moment right now to vote your shares to ensure that your voice is heard in this very important decision regarding your investment.

Enclosed is a research report on the Company prepared by Canaccord Genuity Capital Markets, a global capital markets group with affiliated entities that are members of IIROC/Canadian Investor Protection Fund in Canada and FINRA/SIPC in the United States. We are providing this report so that investors have access to a third party opinion concerning our outlook; however, this report was prepared by Canaccord and CLS did not participate in its preparation.* The research report analyzes the impact of our proposed Massachusetts acquisitions on the Company. In order for us to close on these acquisitions and implement our growth plan, it is critical that shareholders approve the Board’s proposal to increase the number of authorized shares of common stock from 250,000,000 to 750,000,000. This proposal benefits our stockholders in the following ways:

|

● |

Provides Shares for Future Acquisitions. Consolidation is rampant in our industry. We have a pending contract to acquire In Good Health, Inc. in Massachusetts; however, we do not have sufficient remaining shares of authorized stock to complete this acquisition. In addition, we have opportunities to acquire other good-quality businesses, many of which are revenue producing. The authorization of the additional shares does not mean that they will be issued, only that they are available for issuance should the need arise. |

|

● |

Provides Flexibility. The additional authorized shares will also give us flexibility to use shares for future equity financings and general corporate purposes, which could include, among others, strategic partnerships and equity incentive plans. |

The CLS Holdings board of directors unanimously recommends that CLS Holdings stockholders vote “FOR” the amendment to our Articles of Incorporation proposal, and “FOR” the Adjournment Proposal.

Your vote is important. Please vote your shares today by telephone, internet, or by completing and mailing the enclosed proxy card. Remember – every share and every vote counts!

Please make sure your voice is heard in this important matter affecting your investment. If you have any questions, please call MacKenzie Partners, Inc., which is assisting with the solicitation, toll-free at (800) 322-2885 or (212) 929-5500 or at proxy@mackenziepartners.com.

If you have recently voted, please disregard this reminder and thank you for your attention to this important matter.

Sincerely,

CLS Holdings USA, Inc.

* See cautionary language on next page

Safe Harbor / Forward-Looking Statements

Certain of the statements, expectations, and assumptions contained in this letter and the enclosed report are forward-looking statements. Forward-looking statements include, but are not limited to, statements that express intentions, beliefs, expectations, strategies, predictions or any other statements relating to our future activities, financial performance, stock price, issuance of additional stock or other future events or conditions. These statements are not guarantees of future performance and involve risks, uncertainties and assumptions that are difficult to predict and include, without limitation, our expectations as to closing certain transactions. Therefore, actual outcomes and results may, and are likely to, differ materially from what is expressed or forecasted in the forward-looking statements due to numerous factors discussed in the attached report and in documents which we file with the SEC from time to time. In addition, such statements could be affected by risks and uncertainties related to, among other things: our ability to close and integrate certain acquisitions, our ability to successfully implement our business strategy; and other risks described from time to time in periodic and current reports that we file with the SEC. Any forward-looking statements speak only as of the date on which they are made, and except as may be required under applicable securities laws, we do not undertake any obligation to update any forward-looking statements.

|

US Equity Research 22 February 2019 |

Bobby Burleson | Analyst | Canaccord Genuity LLC (US) | BBurleson@cgf.com | 415.229.7163 Jonathan DeCourcey | Associate | Canaccord Genuity LLC (US) | jdecourcey@cgf.com | 617.371.3884 |

|

SPECULATIVE BUY |

Initiation of Coverage

Multi-state play on Massachusetts and Nevada

We are initiating coverage of CLS Holdings USA (CLSH) with a SPECULATIVE BUY rating and a C$1.50 price target. CLSH is a multi-state cannabis operator with planned operations in the legal recreational and medical Massachusetts (MA) and Nevada (NV) cannabis markets. Upon closing key acquisitions, we believe CLSH will be positioned to capitalize on growing demand for legal cannabis in the US through vertical operations including production and dispensaries that are well placed in MA and NV, which we see as two of the more substantial emerging US recreational markets.

Positioned in highly attractive Massachusetts and Nevada markets: With dispensary and production operations planned in both states, CLSH is exposed to what we estimate will be a combined $1.1B retail market in 2019; we conservatively expect the market to grow to $2.1B in 2022, as we look for both states to benefit from cannabis tourism (Massachusetts should attract visitors as the only New England state where recreational marijuana is legal). We believe CLSH’s medical dispensary in MA (In Good Health) appears better positioned to capitalize on the transition to recreational sales compared to recent licensees, given its location close to Boston, parking for 225 cars, and existing cultivation and processing capacity. We expect a recreational license to be awarded to In Good Health in 1H19. In NV, CLSH’s Oasis dispensary is located just off the Strip, accessing tourist and residential foot traffic, with cultivation and processing capacity poised to supply an increasing share of the dispensary’s shelf space.

Production ramp to drive margin expansion: CLSH is targeting a substantial increase in production capacity for both cultivation and processing in MA and NV. As the company grows share of shelf space at its own dispensaries to its targeted 75-80% level from 10-15% today, we anticipate EBITDA margin to expand from 33% to 40% between 2019 and 2020. Given the under-supply situation in MA, where the bulk of CLSH’s revenues in our model are derived (77% in 2019E, 84% in 2020E), we expect CLSH to operate within a relatively stable pricing environment well into 2020.

Rock-bottom valuation reflects need to raise additional capital: CLSH is currently trading at 1.1x EV/EBITDA based on our 2020 estimates. This is substantially below 9.9x for the US peer group. While we expect some multiple expansion for CLSH, especially upon a recreational license award in MA, we are setting a price target multiple of 5.2x EBITDA, well below the peer group average, given CLSH’s need to raise $56M to close outstanding acquisitions and help fund CAPEX and working capital (roughly 92M in share issuance). Our share issuance assumption utilizes an C$0.80 price and anticipates 54% dilution. We note that dilution could be greater if shares are issued at a lower price. However, even if we assume share issuance at the current price our valuation analysis yields a C$0.92 target, which is a significant premium to current levels.

Valuation: Our C$1.50 price target for CLSH is based on a sum-of-the-parts discounted cash flow analysis of the company’s MA and NV operations, including the Brockton and Leicester acquisitions. We use a 12% discount rate, 2% terminal growth rate, and a CAD- to-USD exchange rate of C$1.30/$1.00. Our price target implies an EV/EBITDA multiple of approximately 5.2x our 2020 EBITDA estimate. We believe a SPECULATIVE BUY rating is appropriate given the risks and uncertainties tied to the regulatory environment and the completion of acquisitions. |

||||

|

PRICE TARGET |

C$1.50 |

||||

|

Price (21-Feb) |

C$0.29 |

||||

|

Ticker |

CLSH.U-CSE |

||||

|

|

|||||

|

Market Cap (C$M): |

75.4 |

||||

|

Shares Out., FD (M) : |

260.1 |

||||

|

Enterprise Value (C$M): |

85.2 |

||||

|

FYE Dec |

2018E |

2019E |

2020E |

||

|

Sales (US$M) |

5.1 |

60.5 |

147.7 |

||

|

EBITDA (US$M) |

(14.4) |

19.8 |

58.8 |

||

|

Free Cash Flow (US$M) |

(25.9) |

(36.7) |

18.5 |

||

|

EV/Sales (x) |

12.8 |

1.1 |

0.4 |

||

|

EV/EBITDA (x) |

(4.5) |

3.3 |

1.1 |

||

|

P/Adj. FCF (x) |

(2.2) |

(1.6) |

3.1 |

||

|

Priced as of close of business 21 February 2019 |

|||||

| CLSH is a multi-state cannabis business with planned operations in the Nevada and Massachusetts legal markets. CLSH has significant exposure to retail and production. | |||||

Canaccord Genuity is the global capital markets group of Canaccord Genuity Group Inc. (CF : TSX)

The recommendations and opinions expressed in this research report accurately reflect the research analyst's personal, independent and objective views about any and all the companies and securities that are the subject of this report discussed herein.

For important information, please see the Important Disclosures beginning on page 35 of this document.

|

|

CLS Holdings USA Initiation of Coverage |

| Table of contents | ||

|

Executive summary |

3 |

|

|

Market opportunity |

5 |

|

|

Competitive positioning |

8 |

|

|

Investment risks |

11 |

|

|

Massachusetts market overview |

12 |

|

|

Nevada market overview |

15 |

|

|

Business overview |

16 |

|

|

Valuation |

27 |

|

|

Senior management |

30 |

|

|

Appendices |

||

|

Federal outlook |

32 |

|

|

Key extraction methods |

34 |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 2 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Figure 1: CLS Holdings

Source: Company reports |

Executive summary

We are initiating coverage of CLS Holdings (CLSH) with a SPECULATIVE BUY rating and a C$1.50 price target. CLSH is a multi-state cannabis operator with planned operations in the legal Nevada (NV) and Massachusetts (MA) cannabis markets. Upon closing key acquisitions, we believe CLSH will be positioned to capitalize on growing demand for legal cannabis in the US through vertical operations including production and dispensaries that are well placed in MA and NV, which we consider two of the more attractive US markets. On a combined basis, we estimate MA and NV represent a roughly $1.1BM market, growing 24% through 2022 to reach $2.1B. Further, we expect healthy margin expansion for CLSH through the forecast period as a strong ramp for cultivation and processing capacity in both states allows the company to increasingly supply its own dispensary shelves with flower and branded products. The company also maintains extraction IP that should allow for higher yields as well as additional licensing revenue streams longer-term. Due to uncertainty around the completion of outstanding LOIs, CLSH is trading at a steep discount to the average EV/EBITDA multiple for its US peers on 2020 estimates, roughly 1.1x vs 9.9x, respectively. We expect multiple expansion to occur as CLSH executes its plan and closes key acquisitions, including Leicester and In Good Health before the end of this year.

Our C$1.50 price target for CLSH is based on a sum-of-the-parts discounted cash flow analysis of the company’s Massachusetts and Nevada operations inclusive of the Brockton and Leicester acquisitions. Within our analysis we utilize a 12% discount rate and 2% terminal growth rate along with CAD to USD exchange rate of C$1.30/$1.00. Our price target assumes a share count of 260.1M shares, which includes the current fully diluted share count of 168.4M and the assumption that the company will have to raise capital to fund the In Good Health and Leicester acquisitions and the equity portion of the In Good Health acquisition ($5M in equity inclusive within the total $47.5M acquisition price). Regarding the equity raise, we assume a share price of C$0.80 and a C$1.30/US $1.00 exchange rate, which translates to an additional 91.7M in shares issued. Our C$0.80 estimated share price at the time of issuance reflects a rough midpoint between our price target and the current CLSH share price. Our price target translates to an EV/EBITDA multiple of approximately 5.2x our 2020 EBITDA estimate in CAD.

We believe that there is limited risk that CLSH will be able to raise the necessary capital to fund the acquisitions of the In Good Health and Leicester businesses, and we expect the transactions to close later this year. Nevertheless, we note that the two Massachusetts businesses represent approximately 81% of our sum-of-the-parts valuation analysis. Excluding the acquisitions, our sum-of-the-parts discounted cash flow analysis yields a price target of C$0.31. |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 3 |

|

|

CLS Holdings USA Initiation of Coverage |

Figure 2: Sum-of-the-parts valuation

|

Market Cap (C$M) |

Price Per Share |

Enterprise Value (C$M) |

20E EBITDA ($M) |

20E EBITDA (C$M) |

20E EV/EBITDA |

|||||||||||||||||||

|

Massachusetts |

309.9 | 1.19 | 317.7 | 52.1 | 67.7 | 4.7 | ||||||||||||||||||

|

Nevada |

79.4 | 0.31 | 81.4 | 6.7 | 8.7 | 9.3 | ||||||||||||||||||

|

Total |

389.3 | 1.50 | 399.0 | 58.8 | 76.4 | 5.2 | ||||||||||||||||||

|

Cash ($M) |

14.5 | |||||||||||||||||||||||

|

Cash (C$M) |

18.9 | |||||||||||||||||||||||

|

Debt ($M) |

22 | |||||||||||||||||||||||

|

Debt (C$M) |

28.6 | |||||||||||||||||||||||

|

Shares |

260.1 | |||||||||||||||||||||||

|

Discount Rate |

12% | |||||||||||||||||||||||

|

Terminal Growth |

2% | |||||||||||||||||||||||

Source: Company reports, Canaccord Genuity estimates

|

We note that any variation to our CLSH share price assumption could result in a change to our share count assumption and our price target. At C$0.80, the anticipated share issuance would have a 54% dilutive impact on the number of shares outstanding, while a C$0.25 share price would represent 174% dilution and a C$1.25 share price would have a 35% impact. Within these share price assumptions, our price target would range between C$0.84 and C$1.71. We note that at the current C$0.29 share price, our price target would be C$0.92.

Figure 3: Share issuance sensitivity |

|

Share price at time of equity raise |

Required Share Issuance |

Total Shares |

Price Target (C$M) |

Dilutive Impact |

||||||||||||||

|

C$0.25 |

293.3 | 461.7 | 0.84 | 174 | % | |||||||||||||

|

C$0.50 |

146.6 | 315.0 | 1.24 | 87 | % | |||||||||||||

|

C$0.80 |

91.7 | 260.1 | 1.50 | 54 | % | |||||||||||||

|

C$1.00 |

73.3 | 241.7 | 1.61 | 44 | % | |||||||||||||

|

C$1.25 |

58.7 | 227.1 | 1.71 | 35 | % | |||||||||||||

|

Source: Canaccord Genuity estimates |

||||||||||||||||||

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 4 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Market opportunity

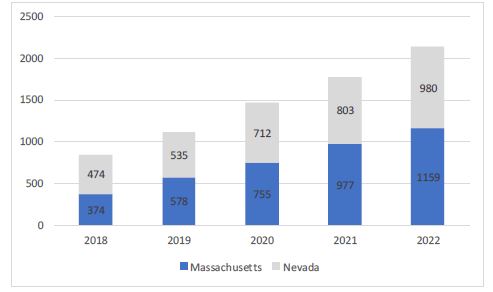

Addressing two of the more attractive US state markets In our view, CLSH has positioned itself to operate in two of the more attractive markets in the country, Massachusetts and Nevada, through a combination of dispensary and cultivation/production assets. With an aggregate market value we peg at nearly $850M in 2018 and conservatively expect to grow to more than $2.1B by 2022, MA and NV offer a combined market CAGR of approximately 20% through our forecast period. While conservative, this growth rate is nevertheless 25% higher than our 16% estimate for the broader US market. Within our 10-year DCF analysis, we anticipate CLSH can maintain a 7% share of the Massachusetts market and a 4% share in Nevada.

Figure 4: MA and NV estimated market value ($M)  Source: Canaccord Genuity estimates |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 5 |

|

|

CLS Holdings USA Initiation of Coverage |

|

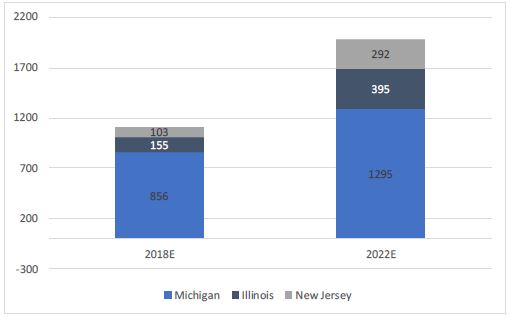

The US Midwest and East Coast offer attractive expansion markets For additional expansion beyond current growth initiatives in CLSH’s core markets, we believe Michigan, Illinois and New Jersey represent likely priorities. With significant existing medical markets, large populations and looming recreational programs (especially in Michigan), these three states offer substantial growth opportunities. We expect CLSH to enter these markets through acquisition of licenses or fully operational businesses. While not yet factored into our model, we estimate these expansion states represented a combined market size of $1.1B in 2018 and project growth to nearly $2.0B in 2022. We note that our projections for 2022 for these three markets could prove conservative as only Michigan factors in a recreational market program rollout, following an initial launch of a recreational program in 2020 following the 2018 approval of recreational sales. Accordingly, Michigan represents the lion’s share of our aggregate market size for the expansion states ($856M or 78% in 2018; $1.3B or 65% in 2022).

Figure 5: Michigan, Illinois and New Jersey market growth projections  Source: Canaccord Genuity estimates |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 6 |

|

|

CLS Holdings USA Initiation of Coverage |

|

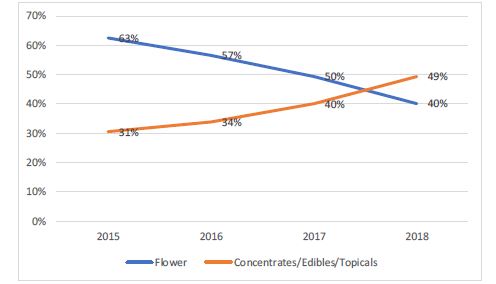

Processing capacity addresses market opportunity as demand shifts away from flower Across its MA and NV operations, CLSH has a combined oil production capacity of 2,400 lbs, which the company expects to grow to 6,600 by 2020. Spending patterns show that new consumers entering the legal cannabis market are less interested in smoking flower, and mature markets such as California, Colorado, Oregon and Washington have exhibited a substantial shift away from flower and toward vape, edibles and other derivative products. According to point-of-sale data compiled by BDS Analytics GreenEdge, in the past four years the sale of edibles, concentrates and topicals has increased from 31% of the market to 49% while the sale of flower has declined from 63% to 40%. If similar adoption levels were to occur in MA and NV, we believe we could expect a market opportunity for products derived from processing that grows from $550M in 2019 to $1.1B by 2022. CLSH’s substantial processing capacity should enhance the company’s ability to supply its retail operations with the appropriate mix of consumer products, as well as brand its own products over time.

Figure 6: Percentage of market by product category (CA, CO, OR, WA)  Source: BDS Analytics GreenEdge |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 7 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Competitive positioning

Solidly positioned to compete through ramping production capabilities and key dispensary assets

Dispensaries well located within attractive state markets Following the formal completion of the In Good Health acquisition, CLSH will own dispensaries in Las Vegas, NV, and Brockton, MA (Oasis and In Good Health, respectively). In Las Vegas, Oasis is adjacent to the Strip, exposing the store to residential and tourist foot traffic. Along with in-store sales, Oasis has a successful delivery business, with home delivery representing approximately 15% of total revenue while yielding an average transaction size 75% higher than its in-store average. In Brockton, In Good Health has a 1,500-sq.-foot medically licensed retail space, servicing approximately 18,000 registered medical patients. The dispensary has been operational since 2015 and was the second medical dispensary in Massachusetts. We expect In Good Health to receive final recreational licenses from the state and city later this month, with recreational sales commencing in the second half of 2019. In our view, Brockton represents one of the more attractive markets in MA for dispensary operations given the city’s significant population of roughly 100k and location only 20 miles from Boston. We expect In Good Health to be well positioned to address recreational demand once its licensing is completed. The dispensary has parking capacity for over 225 cars and an existing cultivation operation for medical marijuana whose capacity would double to support recreational use sales. Moving forward, we anticipate existing and growing operations in the Massachusetts and Nevada markets will serve as the launching point of future expansion initiatives for CLSH. CLSH management brings an extensive background in successfully completing M&A transactions given their significant capital markets and real estate experience, which should help in both targeting acquisition opportunities and in implementing acquired operations.

Figure 7: Planned dispensary assets |

|

Dispensary Operations |

||||||||||

|

Daily Retail Orders |

Current |

Expanded |

||||||||

|

Las Vegas |

350 | 500 | ||||||||

|

Brockton |

275 | 800 | ||||||||

|

Total |

625 | 1,300 | ||||||||

| Source: Company reports, Canaccord Genuity | ||||||||||

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 8 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Expanding cultivation and production footprint to support branded products strategy Based on near-term growth initiatives, including cultivation and production expansion in MA and NV, the completion of acquisitions in MA, and the receipt of licenses for Leicester, CLSH will have a 151,000-sq.-foot cultivation footprint capable of producing approximately 44K lbs. of flower and processing capacity for more than 19K lbs. of oil. We believe this substantial footprint should position CLSH to develop an extensive branded products portfolio for sale through its own dispensaries and on a wholesale basis. Longer term the company anticipates that between 75% and 80% of its dispensary sales will be from internally branded products.

Figure 8: Planned production assets |

|

Flower Production (Lbs) |

Current |

Expanded |

||||||||

| Las Vegas | 2,400 | 6,600 | ||||||||

|

Brockton |

3,400 | 9,000 | ||||||||

|

Leicester |

28,000 | |||||||||

|

Total |

5,800 | 43,600 | ||||||||

|

Processing Capacity (Lbs) |

Current |

Expanded |

||||||||

| Las Vegas | 2,000 | 3,000 | ||||||||

|

Brockton |

1,500 | 3,500 | ||||||||

|

Leicester |

12,600 | |||||||||

|

Total |

3,500 | 19,100 | ||||||||

| Source: Company reports, Canaccord Genuity | ||||||||||

|

Patented extraction capabilities to enhance long term processing position Last year, CLSH was awarded a non-provisional US utility patent for its cannabidiol extraction and conversion process from the US Patent and Trademark Office (US Patent Number 9,950,976 B1). The company’s patented extraction process is believed to result in increased product consistency, to yield higher quality products and to drive cost savings for growers. Specifically, the patented extraction process in lab tests changes the molecular structure of the product and enables the extraction of 2x more delta-nine THC than traditional methods. While the company has not yet commercialized the process, moving forward CLSH plans to generate licensing and fee-for-service revenues through the development of branded concentrates products and through becoming a third-party wholesale processor. We are not yet modeling any licensing or fee revenue from this process. |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 9 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Extraction IP is important source of differentiation within broader processing landscape While cannabis processing can refer to several post-harvesting steps, the term is often used interchangeably with extraction. As the industry develops, independent post- cultivation services are emerging, modeled after the coffee industry. With contract processing services, smaller growers are able to join forces to benefit from economies of scale downstream from harvesting, while continuing to grow their boutique strains. Looking specifically at the extraction step, there are two general categories, cold extraction and heated extraction. Cannabis extracts are used largely for infusing products into edibles and to provide oils and other materials for vaping. Modern heated extraction methods use solvents like butane, methane or CO2, while other methods are hundreds of years old and solvent-free, using various combinations of water, heat, sifting and pressure.

Valuation We utilize a sum-of-parts discounted cash flow analysis of CLHS’s operations in Massachusetts and Nevada inclusive of contributions from the not-yet-completed Brockton and Leicester acquisitions to generate our target valuation for CLSH. Our C$1.50 price target is based on our estimate for a fully diluted share count of 260.1M shares, which includes the company’s current fully diluted share count of 168.4M shares and the assumption that CLSH will issue approximately 91.7M shares to fund the In Good Health and Leicester acquisitions as well as capex needs. We expect the acquisitions to be completed later this year. We note that any variation to our CLSH share price assumption could result in a change to our share count assumption and price target.

Within our price target analysis, we utilize a 12% discount rate, a terminal growth rate of 2% and a CAD to USD exchange rate of C$1.30/US$1.00. We assume that over the long term CLSH can achieve revenues equal to approximately 7% of the Massachusetts market and 4% of the Nevada market. Our price target translates to an EV/EBITDA multiple of approximately 5.2x our 2020 EBITDA estimate in CAD.

Figure 9: Sum-of-the-parts valuation |

|

Market Cap (C$M) |

Price Per Share |

Enterprise Value (C$M) |

20E EBITDA ($M) |

20E EBITDA (C$M) |

20E EV/EBITDA |

|||||||||||||||||||

|

Massachusetts |

309.9 | 1.19 | 317.7 | 52.1 | 67.7 | 4.7 | ||||||||||||||||||

|

Nevada |

79.4 | 0.31 | 81.4 | 6.7 | 8.7 | 9.3 | ||||||||||||||||||

|

Total |

389.3 | 1.50 | 399.0 | 58.8 | 76.4 | 5.2 | ||||||||||||||||||

|

Cash ($M) |

14.5 | |||||||||||||||||||||||

|

Cash (C$M) |

18.9 | |||||||||||||||||||||||

|

Debt ($M) |

22 | |||||||||||||||||||||||

|

Debt (C$M) |

28.6 | |||||||||||||||||||||||

|

Shares |

260.1 | |||||||||||||||||||||||

|

Discount Rate |

12% | |||||||||||||||||||||||

|

Terminal Growth |

2% | |||||||||||||||||||||||

| Source: Company reports, Canaccord Genuity estimates | ||||||||||||||||||||||||

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 10 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Investment risks Risk factors related to the long-term success of CLSH include:

● Capital markets uncertainty: As previously mentioned, CLSH will need to raise capital to fund planned expansion initiatives. Should sentiment or regulations regarding US cannabis operations materially change, it could be difficult (or impractical) for the company to secure additional public market capital.

● Federal prohibition: Cannabis remains federally illegal in the US. CLSH’s existing and targeted acquisitions derive 100% of their revenues from cannabis-touching operations. A change to the federal government’s current hands-off approach to cannabis businesses could result in the cessation of existing operations and curtail expansion. If operations were to cease, shareholders could lose their entire investment.

● Federal legalization: Legalization at the federal level in the near-term could lead to increased competition across CLSH’s operations from better capitalized new entrants, prior to the company’s ability to achieve sufficient scale.

● US state regulations: Adverse changes to state regulations in the states in which CLSH operates could impact performance.

● Massachusetts licensing uncertainty: A significant portion of our near-term financial forecasts depend on the receipt of recreational cannabis licenses in Massachusetts. An extended delay in licensing could adversely impact our estimates and the value of CLSH’s acquisition targets.

● Increased competition: CLSH plans to operate within highly competitive markets. Any unforeseen change in the competitive landscape could hinder the company’s ability to offer products and services as planned and could have an adverse impact on performance.

● Expansion into new markets: The long-term success of CLSH depends in-part on the expansion into developing markets outside of Nevada and Massachusetts. An inability to expand operations into markets in which the company does not currently operate, or the inability of expansion states to develop into markets of sufficient size, could negatively impact future growth.

● Limited operating history: CLSH completed the Oasis (NV) acquisition last June and has a limited history of operating a cannabis business, presenting significant uncertainty regarding operational performance and the company’s ability to hit its financial targets.

● Integration of new businesses: CLSH plans to complete multiple acquisitions in the near term that are expected to be significant contributors to the long-term success of the company. Any unforeseen challenges integrating these businesses could result in an adverse impact to operating results. |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 11 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Massachusetts and Nevada offer substantial prospective growth

Massachusetts: Significant recreational market opportunity Two years after voters approved recreational marijuana in the 2016 election, Massachusetts saw the first recreational marijuana businesses in the state open last November, five months later than originally expected and at a smaller scale. According to industry estimates from BDS Analytics, Massachusetts 2018 total sales were approximately $221M, down approximately 31% from prior estimates for the period of $377M. 2019 market estimates, while down overall (from $604M to $515M in the latest BDS forecast), have been cut at a less dramatic rate and reflect strong Y/Y growth expectations on an uptick in recreational activity this year as the state commences a full-fledged rollout.

The delays in initial rollout last year were attributed to a lack of licensed independent testing labs along with bureaucratic headwinds at both the state and municipal levels. Under the Massachusetts law for recreational cannabis, host communities must sign off on the proposed operation before a license can be issued. Additionally, the municipality can charge a 3% local tax on gross revenues and negotiate a community impact fee for as much as an additional 3% of gross revenues.

While the pace of rollout continues to be slow and largely unpredictable, Massachusetts is expected to quickly become one of the largest cannabis markets in the world due to attractive demographics (6.9M people, blue state) and its position as the first sizable recreational market on the East Coast. The state also has a relatively large existing medical marijuana market, with nearly 65,000 registered patients, and significant pent-up demand, given the slow pace of the rec rollout thus far. We note that once dispensaries open in the Boston metropolitan area, Massachusetts could see a boost from tourism in the next few years with visitors coming from adjacent states in the Northeast. A study by the Colorado Tourism Office from 2016 found that 10% of visitors to Colorado that year came exclusively for legal recreational marijuana. Overall, we continue to forecast the Massachusetts market growing to approximately $1.2B by 2022 and believe this could prove conservative.

Pent-up demand for recreational cannabis in Massachusetts is reflected by the nearly $7M in initial sales at the state’s first two dispensaries in their first three weeks of operation despite the dispensaries largely remote locations (the first two dispensaries located in the less densely populated western part of the state - Leicester and Northampton), limited product availability and high prices. Recreational dispensaries have had to take special measures to handle demand, including the imposition of sales limits per customer and busing in customers from satellite parking lots. We expect delays to ease at the local level moving forward as more communities witness strong demand and reap the associated tax benefits. As of the publishing of this report, Massachusetts has eight operational recreational dispensaries and one additional dispensary licensed to open by the state’s Cannabis Control Commission. Of the dispensaries presently open, only one is located within 25 miles of Boston, with the average distance more than 80 miles from the city center. According to the state’s Cannabis Control Commission there are now 23 total cannabis operations, including testing labs, authorized in Massachusetts (for eleven businesses). |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 12 |

|

|

CLS Holdings USA Initiation of Coverage |

Figure 10: Operational recreational market dispensaries (as of 2/11/2019)

|

Cultivate |

New England Treatment Access (NETA) |

Alternative Therapies Group (ATG) |

Verilife |

Insa |

Theory Wellness |

Temescal Wellness |

Northeast Alternatives |

|

|

Location |

Leicester, MA |

Northampton, MA |

Salem, MA |

Wareham, MA |

Easthampton, MA |

Great Barrington, MA |

Pittsfield, MA |

Fall River, MA |

|

Approx. Distance to Boston |

55 Miles |

100 Miles |

20 Miles |

50 Miles |

120 Miles |

130 Miles |

140 Miles |

55 Miles |

|

Purchase Limits |

Weekends: 1/8 oz. flower, two pre- rolled joints and one edibles package.

|

Up to 1/8 oz flower and three mini pre- rolled joints. |

Up to 1/8 oz.of flower and two vape catridges. |

Up to 1/2 oz. flower and three additional items. |

Up to 1/4 oz. flower, two pre-rolled joints and one product from each other menu category.

|

Up to 1/2 oz. flower and one pre-rolled joint. |

Up to 1/8 oz. flower, two 1/2 gram pre- rolled joints and one vape pen or catridge.

|

None |

|

Opened |

20-Nov-18 |

20-Nov-18 |

15-Dec-18 |

21-Dec-18 |

22-Dec-19 |

11-Jan-19 |

15-Jan-19 |

20-Jan-19 |

Source: Boston.com, company websites, GoogleMaps.

|

Figure 11: Licensed Massachusetts recreational businesses |

|

Alternative Therapies Group |

Retail |

Salem, MA |

|

CDX Analytics |

Independent Testing Laboratory |

Salem, MA |

|

Cultivate Holdings |

Cultivation |

Leicester, MA |

|

Cultivate Holdings |

Production |

Leicester, MA |

|

Cultivate Holdings |

Retail |

Leicester, MA |

|

I.N.S.A |

Cultivation |

Easthampton, MA |

|

I.N.S.A |

Production |

Easthampton, MA |

|

I.N.S.A |

Retail |

Easthampton, MA |

|

MCR Labs |

Independent Testing Laboratory |

Framingham, MA |

|

New England Treatment Access |

Cultivation |

Franklin, MA |

|

New England Treatment Access |

Production |

Franklin, MA |

|

New England Treatment Access |

Retail |

Franklin, MA |

|

Northeast Alternatives |

Cultivation |

Fall River, MA |

|

Northeast Alternatives |

Production |

Fall River, MA |

|

Northeast Alternatives |

Retail |

Fall River, MA |

|

Pharmacannis Massachusetts |

Retail |

Wareham, MA |

|

Revolutionary Clinics |

Cultivation |

Fitchburg, MA |

|

Revolutionary Clinics |

Production |

Fitchburg, MA |

|

Temescal Wellness |

Retail |

Hudson, MA |

|

Temescal Wellness |

Retail |

Pittsfield, MA |

|

Temescal Wellness |

Cultivation |

Worcester, MA |

|

Temescal Wellness |

Production |

Worcester, MA |

|

Theory Wellness |

Retail |

Great Barrington, MA |

| Source: Massachusetts Cannabis Control Commission | ||

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 13 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Healthy price premium likely to persist near-term The head of Massachusetts’ Cannabis Control Commission (CCC) has publicly stated the state should expect four to eight new retail locations per month. We note that there are more than 220 completed business license applications outstanding with the state, according to the CCC. While retailers are the most anticipated segment of cannabis businesses coming online in Massachusetts this year, there is also likely to be a number of non-vertically-integrated operations, including wholesale cultivators and processors and consumer product manufacturers. While over time the addition of non-vertically integrated operators should bring a better balance between supply and demand, we expect pricing to remain largely stable well into 2020 given the degree of pent-up demand and likelihood of significant levels of cannabis tourism. According to Cannabis Benchmarks, wholesale flower is currently priced at $6.29 per gram in Massachusetts, almost 3x the US average and an even greater premium to pricing in mature rec states. The premium at the retail level, while less extreme, is also substantial.

Figure 12: State wholesale and retail pricing ($/G) |

| Wholesale ($/g) | Retail ($/g) | |||||||||

|

MA |

6.29 | 10.00 | ||||||||

|

Relative Price |

||||||||||

|

CA |

236 | % | 137 | % | ||||||

|

CO |

293 | % | 142 | % | ||||||

|

MI |

149 | % | 104 | % | ||||||

|

NV |

158 | % | 121 | % | ||||||

|

OR |

435 | % | 152 | % | ||||||

|

WA |

531 | % | 144 | % | ||||||

|

AZ |

145 | % | 122 | % | ||||||

|

Average |

278 | % | 131 | % | ||||||

| Source: Cannabis Benchmarks, Price of Weed.com | ||||||||||

|

M&A activity underscores attractiveness of Massachusetts market Last month Surterra Wellness acquired New England Treatment Access (NETA), a cannabis business with Massachusetts dispensaries in Brookline (medical only) and Northampton (medical and recreational), and a cultivation facility in Franklin, MA (medical) The acquisition gives Surterra initial exposure to the Massachusetts market and complements the company’s existing operations in Florida, Nevada and Texas. While terms of the acquisition were not disclosed, we believe the deal was one of the largest to date in the US cannabis industry. Since the Surterra announcement, we note that DionyMed Holdings announced a binding agreement to acquire Pioneer Valley Extracts, a cannabis extraction company with a Massachusetts license not yet in operation. We expect additional transactions as larger cannabis companies with production, consumer products, and retail move to gain access to the MA market. |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 14 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Nevada: Strong start for rec program While Massachusetts has been slow to implement a recreational program following the 2016 election, Nevada was quick to enact its program and launched recreational sales in July 2017. Adoption has been rapid, with consumers spending more than $200M in the first six months of operation. The strong start came despite inventory shortages as growers struggled to meet demand and testing requirements and as a limited number of businesses were able to gain appropriate licenses. In Nevada, only existing medical marijuana businesses were able to apply for licenses during the first round of applications, and the number of licenses were capped at 172 until last November when the state held a formal round of licensing. In total, 61 dispensaries were issued conditional licenses by the state, which nearly matched the total number of licenses previously issued (64). Of the licenses issued, 31 were for Clark County (Las Vegas).

According to estimates from BDS Analytics, the market in Nevada grew significantly faster than expected in 2018, reaching an estimated $580M vs. a prior estimate of $369M. In 2019, the market is expected to grow to more than $650M (vs. prior estimate of $481M) on continued strong demand for existing operations and through the addition of newly licensed businesses. While increasing supply as new capacity comes online should drive down prices, so far both wholesale and retail prices in the state have reflected a significant premium to mature recreational markets. In Nevada, the wholesale price per gram of cannabis is currently $3.99 according to Cannabis Benchmarks, significantly above the average price in California ($2.66), Colorado ($2.15), Oregon ($1.45) and Washington ($1.18). Meanwhile the retail price in Nevada is $8.27 per gram, which compares to an average of $6.98 for the western states.

Tourism remains a positive demand driver for the cannabis market in Nevada, and the degree to which it will impact demand is unknown. Over the past ten years Las Vegas has averaged roughly 40M tourists annually, more than 13x the state’s population. We continue to believe that cannabis consumption is complementary to Las Vegas’ broader entertainment offering, and we expect companies in the state to capitalize on strong tourist spending. We believe cannabis companies that build brands in Las Vegas through exceptional retail stores or quality consumer products will be able to propagate those brands into tourist states of origin. Meanwhile, looming changes to local laws may allow cannabis lounges for on-premise consumption, perhaps driving tourist interest in cannabis even further. We believe the first licensed cannabis lounges in Nevada will open this year. We continue to expect the Nevada market to grow to nearly $1B by 2022. |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 15 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Business overview: scaling a multi-state vertically integrated operation

CLS Holdings will be a multi-state cannabis business with operations in Nevada and Massachusetts. CLSH broke into the Nevada market with its acquisitions of Alternative Solutions and Oasis Subsidiaries last June. In Massachusetts, CLSH has locked in an option to acquire a vertically integrated operation with a retail dispensary license for medical sales in Brockton (In Good Health) and has an outstanding non- binding agreement to acquire an 80% stake in a cultivation and production operation in Leicester (with CannAssist). For the In Good Health acquisition, the company will be unable to complete the transaction until November 1 due to a Massachusetts law that requires the acquired business to be established as a for-profit entity for at least one year before acquisition (In Good Health became a for-profit business on November 1, 2018). CLSH is undergoing a transformation into a substantial vertically integrated business, through the completion of the Massachusetts acquisitions, the receipt of recreational licenses for the existing medical businesses in Brockton, the receipt of licenses for the Leicester operation and expansion of cultivation and production assets in both Massachusetts and Nevada. Upon completion of these efforts, CLSH will have dispensary assets capable of fulfilling 1,300 orders per day, a 151,000-sq.- foot cultivation footprint capable of almost 44,000 lbs. of flower production annually, and processing capacity of 19,100 lbs. of flower. With expanded production capacity, CLSH will be positioned to drive substantial share of its own shelf space in its dispensaries (75-80% long term goal) and to build a portfolio of branded products for retail and wholesale distribution. Longer term, the company wants to expand into additional states, primarily in the Midwest (Michigan and Illinois) and Northeast (New Jersey). |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 16 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Figure 13: Substantial vertically integrated operation planned in two states |

|

Dispensary Operations |

||||||||||

| Daily Retail Orders | Current | Expanded | ||||||||

| Las Vegas | 350 | 500 | ||||||||

|

Brockton |

275 | 800 | ||||||||

|

Total |

625 | 1,300 | ||||||||

|

Cultivation (Sq. Footage) |

Current |

Expanded |

||||||||

| Las Vegas | 10,000 | 25,000 | ||||||||

|

Brockton |

20,000 | 40,000 | ||||||||

|

Leicester |

86,000 | |||||||||

|

Total |

30,000 | 151,000 | ||||||||

|

Flower Production (Lbs) |

Current |

Expanded |

||||||||

| Las Vegas | 2,400 | 6,600 | ||||||||

|

Brockton |

3,400 | 9,000 | ||||||||

|

Leicester |

28,000 | |||||||||

|

Total |

5,800 | 43,600 | ||||||||

|

Processing Capacity (Lbs) |

Current |

Expanded |

||||||||

| Las Vegas | 2,000 | 3,000 | ||||||||

|

Brockton |

1,500 | 3,500 | ||||||||

|

Leicester |

12,600 | |||||||||

|

Total |

3,500 | 19,100 | ||||||||

| Source: Company reports, Canaccord Genuity | ||||||||||

|

Forecasting substantial revenue by 2020 with substantial Massachusetts contribution For 2018, we are forecasting approximately $5M in revenues, based on six months of the company’s Nevada operations following the June acquisition of Oasis. For 2019, we are forecasting revenues to grow to approximately $61M on the full-year contribution from the Nevada business and contributions from In Good Health in Brockton. With official completion of In Good Health a technicality (In Good Health must operate as a for-profit business for over one year), CLSH will be able to reflect 2019 YTD results after the close of the acquisition. We expect CLSH to reflect full year Brockton contributions within 2019 fourth quarter results. We are modeling In Good Health to contribute approximately $45M in revenues this year, noting our assumptions include the receipt of an adult use license and the commencement of adult use sales at the dispensary in the second or third quarter. We anticipate Nevada should drive roughly $16M. In 2020, we expect strong growth of 144% Y/Y to approximately $148M, as growth for Nevada and In Good Health is enhanced by revenue from the Leicester cultivation and production business. In NV, we look for Oasis to see higher customer traffic and improving spending levels, while cultivation and manufacturing volumes are expanding for the Las Vegas production operation. A full year of contributions from In Good Health and initial contributions from the Leicester cultivation and production business should also be significant factors. By state, we expect Nevada revenues to grow to $28.5M in 2020, with Massachusetts revenues increasing to $119.1M. |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 17 |

|

|

CLS Holdings USA Initiation of Coverage |

|

We model MA to drive approximately 74% of revenues in 2019, expanding to 81% of total revenue the following year.

Figure 14: Projected revenues by state |

|

Revenue |

2018E |

2019E |

2020E |

|||||||||||

| Massachusetts | 44.7 | 119.1 | ||||||||||||

|

Nevada |

5 | 15.8 | 28.5 | |||||||||||

|

Total |

5 | 60.5 | 147.7 | |||||||||||

|

% of Total Massachusetts |

74% | 81% | ||||||||||||

|

Nevada |

100% | 26% | 19% | |||||||||||

|

Total |

100% | 100% | 100% | |||||||||||

| Source: Canaccord Genuity estimates | ||||||||||||||

|

Increasingly vertically integrated business By business type, we believe retail will represent the largest portion of revenues in 2019 at $33M, as sales at Oasis in Las Vegas are joined by contributions from In Good Health in Brockton for both medical and adult use sales (2H19). Going forward, however, we expect increasing vertical integration with cultivation representing the largest portion of output in our 2020 forecast at 50% of total revenue. We expect strong cultivation revenue growth will come from the addition of the Leicester operation in Massachusetts and a full year of contributions from Brockton, enhanced by expanded capacity at both the Las Vegas and Brockton cultivation facilities. Processing should also account for a growing share of revenues as capacity for oils expands at the Las Vegas facility and through the addition of the Leicester operation. Taken together, we expect Cultivation and Processing to represent just under 70% of total revenue in 2020.

Figure 15: Estimated revenues by business type |

|

2019E |

2020E |

|||||||||

|

Retail |

28.9 | 45.9 | ||||||||

|

Cultivation |

23.7 | 72.1 | ||||||||

|

Processing |

7.9 | 29.6 | ||||||||

|

Total |

60.5 | 147.7 | ||||||||

| Source: Canaccord Genuity estimates | ||||||||||

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 18 |

|

|

CLS Holdings USA Initiation of Coverage |

|

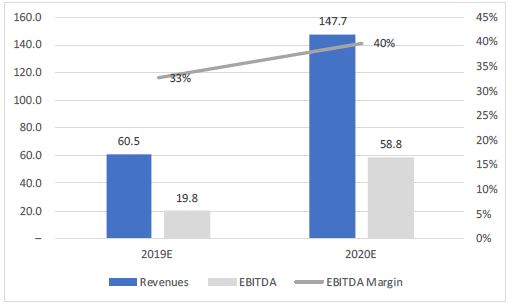

Production ramp positive for margins We note that the mix shift in our model to a greater proportion of Cultivation and Processing revenues drives higher profitability in 2020. By business type, CLSH generates its lowest gross margin from retail operations (approximately 40%) while Cultivation margins track toward the high 40s/low 50s. Processing margins are above 60%. We expect higher revenues from Cultivation and Processing to be a meaningful contributor to margin expansion, and we model gross margin growing from 48% in 2019 to approximately 58% in 2020. Similarly, we estimate EBITDA margin expanding from 33% in 2019 to 40% in 2020 in the face of gross margin expansion on positive mix shift and flattish operating expense as a percentage of revenues. We are modeling 2019 EBITDA of $19.8M, reaching $58.8M in 2020. This compares to a $14M EBITDA loss modeled for 2018.

Figure 16: Revenue and EBITDA forecast ($M)

Source: Canaccord Genuity estimates |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 19 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Figure 17: Oasis Cannabis Dispensary

Source: Company reports

|

Building attractive portfolio of assets in NV and MA

Nevada: Solid retail position; expanding manufacturing capacity Last June, CLSH completed the acquisition of Oasis Cannabis, a vertically integrated cannabis business in Las Vegas, NV. Oasis operates a cultivation and processing business, selling branded concentrates and infused products wholesale under the City Trees brand, as well as retail through its licensed recreational dispensary just off the Strip.

Dispensary operations CLSH’s dispensary in Las Vegas is located within walking distance to the Strip under the name Oasis Cannabis. The 5,000-sq.-foot dispensary is open 24 hours a day and offers delivery services from 10 AM to 8 PM. Home delivery represents approximately 15% of the total sales mix for the Oasis dispensary with an average customer ticket of approximately $100 per order. On average the customer ticket for home delivery is approximately 75% higher than for in-store purchases. Currently, the Oasis location purchases approximately $30K per month in finished product from CLSH’s wholesale business, which represents between 10% and 15% of total retail sales at the store. As CLSH increases production, the company plans to expand internally sourced product to $100K per month.

CLSH intends to grow dispensary revenue in Nevada organically and through acquisitions. At the existing location, management anticipates growing its customer traffic through more advertising focusing in part on driving greater brand awareness. CLSH plans for future acquisitions in Nevada to focus on locations in the state with higher than average median incomes and/or with a significant tourist market. We note that CLSH did not obtain new retail licenses during the latest round of awards completed in December. However, the company is prepared to participate in any subsequent rounds of licensing. With the existing Las Vegas location, management has announced plans for significant improvements, including new signage and an updated store layout. We expect CLSH to generate retail revenue at the Las Vegas dispensary of approximately $7M in 2019, growing to roughly $10M in 2020 as the company expands the number of orders per day (413 target for 2019; 500 target for 2020) and increases average customer ticket to $55 in 2020 from $49 this year.

Figure 18: Las Vegas dispensary operations projections |

|

2019 |

2020 |

|||||||||

|

Orders per day |

413 | 500 | ||||||||

|

Average order size |

48.8 | 55 | ||||||||

|

Days |

360 | 360 | ||||||||

|

Revenue |

7.3 | 9.9 | ||||||||

|

Source: Canaccord Genuity estimates |

||||||||||

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 20 |

|

|

CLS Holdings USA Initiation of Coverage |

|

|

City Trees wholesale production CLSH operates a wholesale business located in North Las Vegas, NV, under the name City Trees. The business primarily consists of the production and sale of branded products manufactured from distilled cannabis oil purchased from third party suppliers. Moving forward as the company expands its cultivation facilities, City Tree is expected to extract cannabis oils internally. City Trees has approximately twenty-five customers in the Las Vegas and Reno markets, and currently grows only breeding stock, with all raw materials sourced from third parties. Manufactured products include branded vaporizers (City Tree brand), CBD- and THC-infused capsules (City Caps brand), and a recently launched line of tinctures.

Expanding capacity in 1H19 CLSH’s growth strategy for its wholesale business is focused on the build-out of the existing wholesale cultivation and production facility. In 2019, CLSH plans to complete a Phase One expansion with additional expansion initiatives to follow. Phase One will cost an estimated $3M and is expected to be completed in the second quarter. The expanded capacity should contribute to both top and bottom line results, with the company expecting to capture higher margins on internal supply and production.

Growing revenue across flower and branded products We expect CLSH to generate approximately $6M in revenues from cultivation with the City Trees operation this year, growing to roughly $15M in 2020 on increased production from the expanded capacity. Within our model, we assume the company will nearly triple the amount of flower produced Y/Y from 2,400 lbs in 2019 to 6,600 in 2020. Meanwhile, as CLSH expands processing at the City Trees facility we are forecasting manufacturing revenues to grow from $2.5M this year to $3.8M in 2020 as the company increases the production of oil from 300 to 450 lbs. We assume an average price of $18.50 per gram for processed oil, or roughly $8,400 per pound.

Figure 19: Nevada cultivation and manufacturing estimates |

|

Cultivation |

2019 |

2020 |

||||||||

|

Flower produced (lbs) |

2,400 | 6,600 | ||||||||

|

Revenue |

$ | 6.0 | $ | 14.9 | ||||||

|

Processing |

2019 |

2020 |

||||||||

|

Capacity (lbs/yr) |

2,000 | 3,000 | ||||||||

|

Yield |

15% | 15% | ||||||||

|

Oil Produced (Lbs) |

300 | 450 | ||||||||

|

Revenue |

$ | 2.5 | $ | 3.8 | ||||||

|

Source: Canaccord Genuity estimates |

||||||||||

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 21 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Figure 20: In Good Health  Source: Company reports |

Massachusetts: transitioning from medical to recreational retail; expanding production

Last fall, CLSH entered into separate non-binding agreements to acquire two cannabis businesses in Massachusetts. The to-be-acquired businesses consist of a vertically integrated operation located in Brockton with cultivation, production and dispensary assets (In Good Health) and a cultivation and extraction facility in Leicester (JV with CannAssist).

In January, CLSH entered into an option to acquire In Good Health, with the acquisition expected to be completed in November 2019 when the acquired business has been a for-profit entity for more than one year. Meanwhile the Leicester investment remains an outstanding LOI and dependent on receipt of final licenses to operate.

In Good Health On October 31, CLSH entered into an agreement whereby the company loaned In Good Health Inc. $5M at 6% annual interest for a three-year period in exchange for the exclusive option to purchase In Good Health for $47.5M in total consideration ($35M cash, $7.5M in five-year promissory notes and $5M in common stock). Relative to the current run rate of revenues ($1M per month), the acquisition price is approximately 4x last year’s sales. The acquisition agreement is locked in and CLSH will be able to officially close the transaction in November when In Good Health has been in operation as a for-profit entity for over one year. We note that as previously discussed, the company will have to raise additional capital in order to complete the transaction.

In Good Health currently operates a 1,500-square-foot medical marijuana dispensary located in Brockton and a wholesale cultivation and production business on site. In Good Health opened in 2015 and was the second medical dispensary to be operational in Massachusetts. Last February In Good Health commenced wholesale production operations. The dispensary serves approximately 18,000 registered patients and delivers to more than 200 homes. In Good Health generates an average ticket of $125 at the dispensary and $300 on deliveries, with capacity to serve between 800 and 1,000 customers daily under the existing footprint.

Strong position for recreational retail sales As a medical-only dispensary, In Good Health generates approximately $1M in monthly revenues. The company has applied for a recreational license and is awaiting receipt of final approval. A vote by the city of Brockton to approve recreational cannabis businesses is expected to come on February 28, and the local commissions have stated that they are in favor of the licensing. With the city of Brockton open to recreational marijuana sales, we expect In Good Health to be licensed and operating as a recreational business by the second half of this year. Of note, with more than 225 parking and meaningful existing capacity to produce medical marijuana, we expect In Good Health to be better positioned to satisfy recreational demand than other recently licensed operations in Massachusetts. Longer term, CLSH intends to expand retail sales in MA through the acquisition of existing dispensaries and organic development of new retail stores. |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 22 |

|

|

CLS Holdings USA Initiation of Coverage |

|

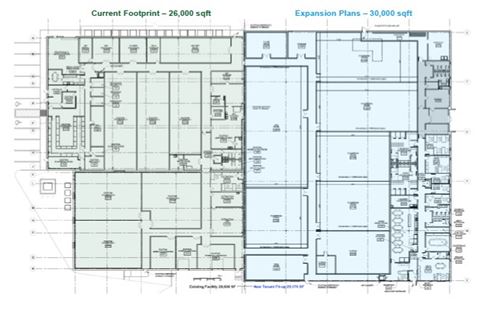

Expanding production capacity In addition to dispensary operations, In Good Health operates a 26,000-square-feet cultivation and production facility, of which 20,000 sq. feet is dedicated to cultivation. Currently the company produces at a rate of 3,400 lbs. of flower per year, of which approximately 1,200 lbs. is allocated for extraction. CLSH has significant expansion plans for the In Good Health operation, and by the second half of this year In Good Health is expected to add approximately 30,000 square feet of cultivation and extraction space and increase production space to 2,000 sq. feet from a 1,000 sq. ft. current footprint and annual flower production capacity to more than 9,000 lbs. In conjunction with the expansion, production capacity for oil will increase from 1,500 lbs. of concentrates annually to more than 3,500 lbs. Manufactured products include: concentrates, edibles, flower, infused water, pre-rolls, tinctures and vape products. The company produces extracts, edibles and infused water under the Infinity Brand and is the exclusive distributor in the state of Massachusetts for Manna transdermal patches, PAX vape pens, and Quicksilver sublingual products. The exclusive distribution agreement runs through 2020.

Figure 21: In Good Health near-term expansion

Source: Company reports |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 23 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Revenue growth split across retail and production We expect In Good Health operations to contribute approximately $52M in revenues this year, to be reflected entirely in the fourth quarter due to the timing of the official acquisition close. For 2020, we are forecasting revenues from In Good Health to increase to nearly $77M. By business type, we believe dispensary sales will represent the largest portion of revenues over the next two years at $21.7M and $36M, respectively. Meanwhile, we are forecasting revenues this year and next for cultivation to be $17.7M and $26.3M, and processing revenues to be $5.4M and $10.6M.

Figure 22: In Good Health estimates |

|

Dispensary Orders per day |

2019E |

2020E |

||||||||

| 481 | 800 | |||||||||

|

Average order size |

125 | 125 | ||||||||

|

Days |

360 | 360 | ||||||||

|

Revenue |

21.7 | 36.0 | ||||||||

|

Cultivation |

||||||||||

|

Footprint (sq. ft) |

40,000 | 40,000 | ||||||||

|

Flower produced (lbs) |

5,450 | 9,000 | ||||||||

|

Revenue |

$ | 17.7 | $ | 26.3 | ||||||

|

Processing |

||||||||||

|

Capacity (lbs/yr) |

2,375 | 3,500 | ||||||||

|

Yield |

0 | 0 | ||||||||

|

Oil produced (g) |

134,498 | 266,158 | ||||||||

|

Revenue |

$ | 5.4 | $ | 10.6 | ||||||

| Source: Canaccord Genuity estimates | ||||||||||

|

Figure 23: CannAssist

Source: Company reports |

CannAssist

In September, CLSH entered into a non-binding LOI to acquire an 80% interest in a CannAssist project in Leicester, MA, for total cost of approximately $25M. The termination date for the Leicester acquisition is July 1, 2019. As previously mentioned, CLSH will need to raise capital in order to fund the Leicester acquisition.

For CannAssist, the CLSH investment will fund the construction of a cultivation and extraction facility at the company’s Leicester location. CannAssist has been approved by the host community but is currently unlicensed in the state. The acquisition agreement is contingent on CannAssist receiving state level approval to grow and sell cannabis. To date, all local approvals have been received and construction on the facility is expected to begin in the first quarter. We expect the company to receive a license and for the acquisition to close this year with contributions from operations coming in 2020. The planned buildout at the Leicester facility is designed to yield up to 28,000 lbs. of flower annually and be capable of processing up to 12,600 lbs. of flower and trim per year. Upon completion, the Leicester facility would be the third largest in Massachusetts based on existing operations in the state. |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 24 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Revenue contribution by 2020 As previously mentioned, we do not expect revenue contributions this year from the CannAssist business. However, we believe the operation will be running at full capacity by 2020. CLSH management expects the facility to be operational and produce its first harvest in the fourth quarter of this year. We are forecasting revenues from 80% interest in the CannAssist business of approximately $46M in 2020, $30.9M from cultivation and $15.2M from processing.

Figure 24: Leicester, Massachusetts, cultivation and extraction facility  Source: Company reports

Future acquisition targets focused in Midwest and East Coast of US With Brockton and Leicester establishing a beachhead on the East Coast that would complement the existing Nevada businesses, the company plans to target additional growth through acquisition within MA and NV and in additional states primarily in the Midwest and on the East Coast. Management has discussed ideal targets being existing mid-sized businesses capable of generating $1M in monthly revenues, with room to grow to between $4M and $5M in short order with an infusion of capital. We believe New Jersey, Illinois and Michigan are potential states for near term expansion. We see these three states offering a significant market opportunity in the years ahead, believing they will approximate a combined $1.9M by 2022, even before factoring recreational programs that could emerge in Illinois and New Jersey. A successful expansion into these three states would nearly double the company’s 2022 addressable market, according to our estimates. |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 25 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Pro forma cap table based on additional funding needs CLSH currently has approximately $14.5M in cash on its balance sheet. Over the next year we expect the company to invest approximately $4M in the build-out of Nevada cultivation capacity and require $6.9M to fund working capital needs. Additionally, to fund the In Good Health and Leicester acquisitions, CLSH will need to issue approximately 83.5M shares (based on our assumed C$0.80 issuance price point) to fund the required cash portion of the acquisitions and has committed to issue approximately $5M in equity in conjunction with the In Good Health acquisition (which translates to an additional 8.1M shares). As previously noted, our C$0.80 share issuance price assumption reflects an approximate midpoint between our price target and the stock’s current share price. In total, following a required capital raise we are modelling CLSH to have a fully diluted shares outstanding of 260.1M.

Figure 25: Required share issuance |

|

Cash ($M) |

14.5 | |||||

|

Nevada Cultivation Expansion ($M) |

4.0 | |||||

|

Working Capital Requirements ($M0 |

6.9 | |||||

|

In Good Health ($M) |

30.0 | |||||

|

Leicester ($M) |

25.0 | |||||

|

Cash Required ($M) |

51.4 | |||||

|

Cash Required (C$M) |

66.8 | |||||

|

Shares at C$0.80 |

83.5 | |||||

|

Equity Portion of In Good Health Acquistion ($M) |

5 | |||||

|

Equity Portion of In Good Health Acquistion ($CM) |

6.5 | |||||

|

Shares at C$0.80 |

8.1 | |||||

|

Total Additional Shares |

91.7 | |||||

| Source: Company reports, Canaccord Genuity estimates | ||||||

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 26 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Figure 26: Pro forma capitalization table |

|

Basic shares outstanding |

126.2 | |||||

|

Warrants |

42.2 | |||||

|

Current Fully Dilutive Shares Outstanding |

168.4 | |||||

|

Shares to be Issued at C$0.80 |

91.7 | |||||

|

Totally Assumed Fully Dilutive Shares |

260.1 | |||||

|

CLSH Share Price (C$) |

0.29 | |||||

|

Market Cap (C$M) |

74.1 | |||||

|

Cash (C$M) |

18.9 | |||||

|

Debt (C$M) |

28.6 | |||||

|

Enterprise Value (C$M) |

83.9 | |||||

| Source: Company reports, Canaccord Genuity estimates | ||||||

|

Valuation: substantial discount to US peer average

Sum-of-the-parts valuation We utilize a sum-of-parts discounted cash flow analysis of CLHS’s operations in Massachusetts and Nevada inclusive of contributions from the not-yet-completed Brockton and Leicester acquisitions to derive our C$1.50 price target. Our DCF analysis assumes a fully dilutive share count of 260.1M shares, which includes the company’s current fully diluted share count of 168.4M shares and the assumption that CLSH will issue approximately 91.7M shares to fund the In Good Health and Leicester acquisitions as well as near term capex needs. We expect the acquisitions to be completed later this year. Within our share count estimate we expect that the company will be able to raise the required capital at a share price of C$0.80 and assume a C$1.30/US $1.00 exchange rate. We note that any variation to our CLSH share price assumption could result in a change to our share count assumption and price target.

For our price target analysis, we utilize a 12% discount rate, a terminal growth rate of 2% and a CAD to USD exchange rate of C$1.30/US$1.00. We assume that over the long term CLSH can achieve revenues equal to approximately 7% of the Massachusetts market and 4% of the Nevada market. Our price target translates to an EV/EBITDA multiple of approximately 5.2x our 2020 EBITDA estimate in CAD.

As previously noted, while we believe that there is limited risk that CLSH will be able to raise the necessary capital to fund the acquisitions of the In Good Health and Leicester businesses and expect the transactions to close later this year, we note that the two Massachusetts businesses represent more than 80% of our sum-of-the-parts valuation analysis. Excluding the acquisitions, our sum-of-the-parts discounted cash flow analysis derives a price target of C$0.31. |

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 27 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Figure 27: Sum-of-the-parts valuation |

|

Market Cap (C$M) |

Price Per Share |

Enterprise Value (C$M) |

20E EBITDA ($M) |

20E EBITDA (C$M) |

20E EV/EBITDA |

|||||||||||||||||||

|

Massachusetts |

309.9 | 1.19 | 317.7 | 52.1 | 67.7 | 4.7 | ||||||||||||||||||

|

Nevada |

79.4 | 0.31 | 81.4 | 6.7 | 8.7 | 9.3 | ||||||||||||||||||

|

Total |

389.3 | 1.50 | 399.0 | 58.8 | 76.4 | 5.2 | ||||||||||||||||||

|

Cash ($M) |

14.5 | |||||||||||||||||||||||

|

Cash (C$M) |

18.9 | |||||||||||||||||||||||

|

Debt ($M) |

22 | |||||||||||||||||||||||

|

Debt (C$M) |

28.6 | |||||||||||||||||||||||

|

Shares |

260.1 | |||||||||||||||||||||||

|

Discount Rate |

12% | |||||||||||||||||||||||

|

Terminal Growth |

2% | |||||||||||||||||||||||

|

Source: Company reports, Canaccord Genuity estimates |

||||||||||||||||||||||||

|

We note that any variation to our CLSH share price assumption could result in a change to our share count assumption and price target. At C$0.80, the anticipated share issuance would have a 54% dilutive impact on the number of shares outstanding, while a C$0.25 share price would represent 174% dilution and a C$1.25 share price would have a 35% impact. Within these share price assumptions, we note that our price target could range between C$0.84 to C$1.71.

Figure 28: Share issuance sensitivity |

|

at time of |

Issuance |

Total Shares |

Target |

Impact |

||||||||||||||

|

C$0.25 |

293.3 | 461.7 | 0.84 | 174 | % | |||||||||||||

|

C$0.50 |

146.6 | 315.0 | 1.24 | 87 | % | |||||||||||||

|

C$0.80 |

91.7 | 260.1 | 1.50 | 54 | % | |||||||||||||

|

C$1.00 |

73.3 | 241.7 | 1.61 | 44 | % | |||||||||||||

|

C$1.25 |

58.7 | 227.1 | 1.71 | 35 | % | |||||||||||||

|

Source: Canaccord Genuity estimates |

||||||||||||||||||

|

Speculative Buy Target Price C$1.50 | 22 February 2019 |

Cannabis 28 |

|

|

CLS Holdings USA Initiation of Coverage |

|

Relative valuation On an EV/EBITDA basis, CLSH stock is currently trading at a multiple of 1.1x our 2020 estimate while on an EV/Revenue basis the stock is trading at 0.4x our 2020 estimate. Current CLSH multiples represent a significant discount to a peer group of US operators currently trading at an average EV/EBITDA multiple of 10x 2020 estimates and EV/Revenue multiple of 2.9x. |

Figure 29: Peer group analysis

|

Ticker |

Share |

Market |

EV/EBITDA |

EV/Revenue |

|||||||||||||||||

|

Price |

Cap (M) |

CY 2019 E |

CY 2020 E |

CY 2019 E |

CY 2020 E |

||||||||||||||||

|

CLS Holdings |

CLSH |

0.29 | 74 |

3.3x |

1.1x |

1.1x |